Introduction

As of October 24, 2025, global financial markets are presenting a dynamic landscape influenced by various factors including trade tensions, geopolitical uncertainties, and fluctuations in the energy sector. Investors are navigating a period highlighted by shifting market sentiments, which have been notably affected by recent developments in international trade agreements and regulatory changes across major economies.

The prevailing mood among investors reflects caution, driven by ongoing trade disputes that have escalated between major powers, notably affecting the flow of goods and services. Trade tensions, particularly between the United States and China, have prompted market participants to reassess their strategies and investment allocations. These disputes may not only impact bilateral trade but also have broader repercussions on global supply chains and economic growth prospects.

Moreover, the energy market is undergoing significant transformations as shifts in demand and supply dynamics are reshaping pricing strategies and investment decisions. Recent geopolitical events in oil-producing regions have led to volatility in crude oil prices, further impacting stock markets worldwide. The energy sector’s wrestling with clean energy transitions alongside traditional fossil fuel reliance continues to compound uncertainties for investors looking at long-term sustainability and returns.

Additionally, central banks across various countries are adapting their monetary policies in response to these shifting landscapes. Interest rates remain a crucial focus as policymakers strive to strike a balance between supporting economic growth and controlling inflationary pressures, particularly amid evolving global conditions.

Overall, the global financial markets stand at a pivotal point, where a confluence of trade dynamics and energy market movements are set to determine the trajectory of investments and economic health in the near future. Understanding these factors will provide valuable insights as investors prepare to navigate the ever-changing market terrain.

Recent Market Sentiment

In the past 24 hours, there has been a notable shift in market sentiment, as investor confidence has turned predominantly bearish. This change appears to be driven by several factors, with a significant focus on geopolitical tensions and the evolving status of US-China trade relations. Historically, volatile geopolitical landscapes have had the potential to adversely affect investor sentiment, and the current environment is no exception.

Key indicators show that uncertainties surrounding trade policies and negotiations between the United States and China have escalated. Recent discussions have revealed a lack of consensus on critical issues, which has raised concerns among market participants. The lingering questions around tariffs, intellectual property protections, and technology transfers have all contributed to a pervasive sense of unease. This hesitation is reflected in various segments of the financial markets, leading to sell-offs in tech stocks, which are often viewed as sensitive to trade developments.

Moreover, economic data released recently has also played a role in shaping market perceptions. Reports indicating sluggish economic growth in both nations have heightened fears regarding supply chain disruptions and overall economic stability. As a result, many investors are reassessing their portfolios and cautiously adjusting their positions in anticipation of further volatility. The flight to safer assets, such as government bonds and precious metals, underscores this shift in strategy, indicating a retreat from riskier investments.

As market sentiment turns increasingly bearish, it is essential for investors to remain vigilant and informed about ongoing developments, particularly those relating to US-China trade relations. The implications of this sentiment shift may lead to a more cautious approach to trading decisions, with an emphasis on risk management strategies. Understanding the root causes of this negative sentiment will be crucial for navigating the complex landscape of financial markets in the coming weeks.

US Stock Market Performance

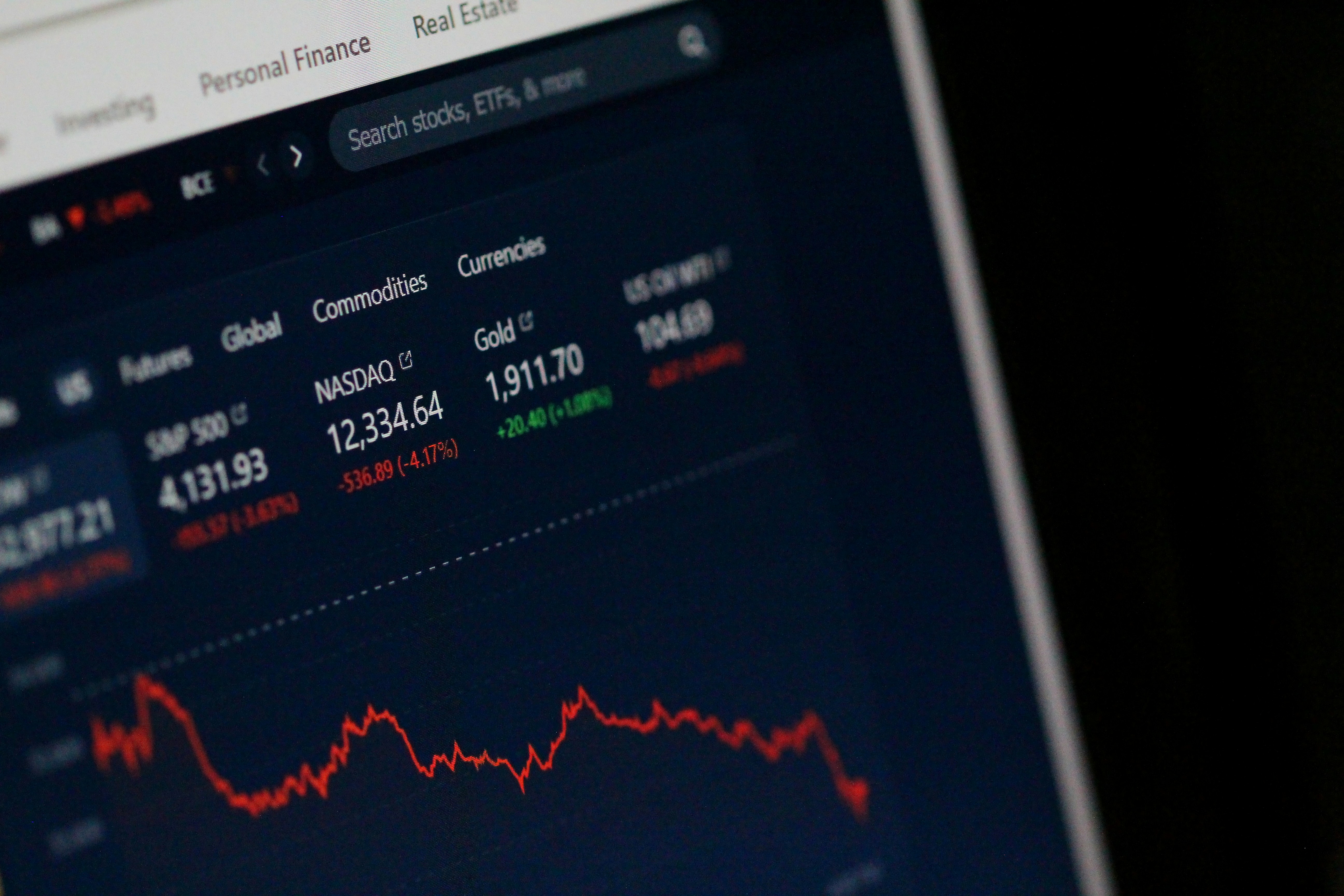

On October 23, 2025, the major US stock indices exhibited a notable decline during the trading session. The Dow Jones Industrial Average (DJIA) fell sharply, closing down by approximately 2.3%. This reduction in value was significantly impacted by key factors such as economic concerns and fluctuations in investor sentiment. Stocks within the DJIA displayed varied performances, with companies like Boeing and Caterpillar facing notable losses, contributing heavily to the overall decline of the index.

Meanwhile, the NASDAQ Composite, heavily weighted towards technology stocks, also suffered on this day, experiencing a decrease of around 3.1%. This marked one of the more significant declines for technology-focused stocks, driven largely by disappointing earnings reports from major players in the sector. Specifically, companies like Apple and Amazon reported results that were below analysts’ expectations, leading to a sharp sell-off among investors, which significantly pressured the overall index.

The S&P 500, representing a broader section of the US stock market, mirrored these declines, finishing the day with a loss of approximately 2.8%. The downturn was pervasive across various sectors, including consumer discretionary and healthcare, indicating a widespread bearish sentiment among investors. As the financial markets reacted to the potential implications of rising interest rates and geopolitical tensions, trading volumes surged, reflecting heightened volatility.

Overall, the performance of the major US stock indices on October 23, 2025, underscores a turbulent environment characterized by uncertainty and reactionary trading. Investors remain vigilant in monitoring developments that could further influence market dynamics in the near term.

Impact of US-China Trade Tensions

The ongoing trade tensions between the United States and China have been a significant point of concern for global financial markets, particularly as these two major economies continue to exert influence over international trade policies. In recent months, there have been several developments that have exacerbated these tensions, including the introduction of new tariffs, restrictions on technology transfers, and increased scrutiny of Chinese firms operating in the US. As a result, investor sentiment has become increasingly cautious, leading to volatility in stock markets worldwide.

One of the major concerns among investors is the potential for a prolonged economic downturn fueled by these trade disputes. As companies grapple with uncertainty regarding supply chains and investment strategies, many are reconsidering their operations in both countries. This uncertainty has tended to dampen market recovery efforts, as businesses are less likely to expand or invest in new projects when faced with unpredictable trade policies. Additionally, industries that rely heavily on exports or are deeply integrated into global supply chains have been particularly impacted by fluctuations in trade relations.

Moreover, the repercussions of US-China trade tensions extend beyond bilateral relations, influencing global market dynamics. For example, emerging markets often find themselves caught in the crossfire of these disputes, leading to increased volatility in currencies and commodity prices. Investors are keeping a close eye on policy changes, as any escalation of tensions could lead to further economic disruptions. Consequently, financial analysts are advising caution, emphasizing the importance of remaining vigilant about geopolitical developments as they navigate the complexities of the current market environment. The ongoing trade conflict remains a pivotal factor in shaping economic forecasts and market strategies going forward.

Energy Market Movements

The energy market has experienced significant fluctuations recently, particularly driven by a notable surge in oil prices. As of October 24, 2025, the price of crude oil has risen markedly, crossing thresholds that many analysts had not anticipated. This spike in oil prices has been influenced by several interconnected factors, with the implementation of new US sanctions against Russia being a pivotal element. These sanctions not only restrict the flow of Russian oil into global markets but also create a climate of uncertainty that often results in upward pressure on prices.

In addition to geopolitical tensions, the global demand for oil remains robust, exacerbating the situation. As economies around the world continue to recover from the impacts of the pandemic, the resurgence in industrial activities has led to increased oil consumption. This sustained demand, juxtaposed with the supply constraints resulting from sanctions and other production-related disruptions, has set the stage for rising oil prices. Furthermore, investor sentiment has been affected by these developments, leading to a preference for energy stocks, which many perceive as a hedge against inflationary pressures driven by the increasing costs of crude oil.

As a direct consequence of the rising oil prices, energy stocks have demonstrated significant volatility. Stocks in major oil companies have experienced increases in their valuations, as investors seek to capitalize on the anticipated profit growth linked to higher oil prices. The energy sector overall has seen a positive response, with many investors focusing on renewables and alternative energy sources alongside traditional oil and gas investments. The recent energy market dynamics highlight the complex interplay between geopolitical events, supply and demand factors, and investor behavior, thereby underscoring the intricate nature of global financial markets.

Sector Performance Analysis

As of October 24, 2025, the performance of various sectors within the global financial markets presents a complex landscape characterized by stark contrasts. With equities facing bearish trends, many investors have adopted a cautious stance, seeking refuge in sectors demonstrating resilience amid economic uncertainty. In this context, a comparative analysis reveals that not all sectors have suffered equally; in fact, the energy sector has emerged as a notable exception.

The continued reverberations of geopolitical tensions, along with fluctuating commodity prices, have significantly influenced market sentiment. Energy stocks, buoyed by rising oil prices attributable to continued demand and supply constraints, have exhibited bullish trends. This uplift in the energy sector provides insight into potential investment opportunities for risk-averse investors exploring diversification strategies. Through a focus on key energy companies, portfolios can benefit from the momentum seen within this domain, especially when broader market factors prompt volatility.

In contrast, the technology and consumer discretionary sectors have seen increased pressure, primarily as market participants react to tighter monetary policies and inflationary pressures. These sectors, traditionally viewed as growth-oriented investments, have been subject to downward revisions in earnings estimates. Such bearish judgments have led to sharp declines in share prices, allowing value-oriented investors to seek opportunities at lower entry points, despite the uncertain outlook.

Furthermore, the financial sector reflects a mixed performance, where banks and financial services firms grapple with margin compression while looking to benefit from higher interest rates. As such, savvy investors may consider sector rotation strategies, capitalizing on the dichotomy between bearish equity performance and the relative strength seen in energy stocks.

Overall, with a comprehensive understanding of the dynamics at play, investors can navigate the current landscape, identifying resilient sectors while remaining cognizant of the prevailing economic conditions.

Global Market Reactions

The global financial landscape in October 2025 is marked by pronounced bearish sentiment, which is significantly impacting international markets outside of the United States. Both European and Asian markets are navigating the complexities posed by fluctuating energy prices, geopolitical tensions, and economic uncertainties. In Europe, indices such as the FTSE 100 and the DAX have experienced notable declines, reflecting widespread investor apprehension. Energy dynamics, particularly the volatility in oil and gas prices due to ongoing conflicts and production adjustments, are core factors affecting market performance.

The European Central Bank’s (ECB) recent interest rate decisions exacerbate the situation, as investors weigh the implications of tighter monetary policy against the backdrop of surging inflation rates. As a result, sectors reliant on consumer spending, such as retail and automotive, have faced considerable headwinds. The resilience of the European markets is being tested, with financial planners and analysts closely scrutinizing the data for signs of stabilization amidst the prevailing uncertainty.

On the Asian front, markets exhibit varied responses influenced by national policies and local conditions. For instance, Japan’s Nikkei 225 has shown signs of volatility as it grapples with the aftereffects of the yen’s depreciation and supply chain disruptions. Conversely, Chinese markets are responding more robustly to government stimulus measures aimed at rejuvenating economic growth, although underlying challenges persist, such as property sector weaknesses and regulatory crackdowns. The dichotomy in response across the region highlights the distinct economic conditions, which require tailored investment strategies.

Investor sentiment across these regions emphasizes caution, driven by a complex interplay of localized influences. Market participants are increasingly focused on adaptive strategies to navigate these turbulent waters, as uncertainty in global financial markets continues to play a pivotal role in shaping economic trajectories worldwide.

Economic Indicators to Watch

As investors navigate the complexities of global financial markets, monitoring key economic indicators becomes crucial for informed decision-making. Among these indicators, trade figures, consumer confidence, and manufacturing outputs play pivotal roles in shaping market trends and future expectations.

Trade data, especially import and export figures, can provide insight into the health of national economies. A rising trade deficit may indicate weakening domestic demand, potentially leading to currency depreciation. Conversely, a trade surplus could signal strong export performance and bolster market confidence. Investors should particularly note quarterly reports as they can influence economic policies and investor sentiment, particularly in major economies like the United States, China, and the European Union.

Another vital economic indicator is consumer confidence, which reflects consumers’ willingness to spend. High consumer confidence typically correlates with increased consumer spending, thus stimulating economic growth. The Consumer Confidence Index (CCI) is a widely regarded metric, offering insights into how consumers perceive economic conditions. Significant fluctuations in this indicator can have ripple effects in financial markets, as higher consumer spending tends to bolster company revenues and stock prices.

Manufacturing output also serves as a critical gauge of economic health. The Purchasing Managers’ Index (PMI) specifically focuses on manufacturing activity, providing insights into whether the sector is expanding or contracting. A PMI above 50 indicates growth, while a figure below signifies contraction. Deviations from expected manufacturing outputs can lead to market volatility, making this indicator a key focal point for investors.

As economic conditions continually evolve, keeping a close eye on these indicators will help investors anticipate market shifts and make well-informed investment choices. By understanding the interplay between trade, consumer sentiment, and manufacturing, stakeholders may better navigate the opportunities and risks present in global financial landscapes.

Market Predictions

As we assess the current market sentiment and underlying economic conditions, several analysts are beginning to formulate predictions about potential future movements in both the stock and energy markets. Recent trends indicate a cautious optimism surrounding the equity markets, driven by robust corporate earnings and positive economic indicators—particularly in the technology and consumer discretionary sectors. Analysts project that, barring any significant geopolitical disruptions or unexpected shifts in economic policy, the stock market may continue to experience moderate gains. This outlook is underpinned by historical performance patterns during similar economic cycles, suggesting a potential for steady growth in the near term.

In the energy sector, predictions remain more varied due to the multifaceted influences affecting oil and gas prices. Factors such as OPEC’s production decisions, changes in global demand, and evolving energy policies significantly shape market dynamics. Current forecasts suggest that crude oil prices might stabilize in the short term, particularly if OPEC maintains its production cuts in response to fluctuating demand arising from new COVID-19 variants and their impact on global travel and consumption. Furthermore, with greater investments in renewable energy and technological innovations, the energy market is likely to undergo transformative shifts that could lead to volatility but also opportunities for growth.

Additionally, it is essential to consider potential scenarios that may unfold in the forthcoming months. For instance, if inflation persists beyond current expectations, central banks may be prompted to adopt more aggressive monetary policies, impacting both stock and energy markets significantly. Conversely, if consumer confidence improves and economic activity accelerates, there could be an upward trajectory for market valuations. In conclusion, while there are several plausible scenarios for the upcoming months, the intricate interplay of various economic factors will ultimately determine the direction of financial markets, necessitating close monitoring by investors and stakeholders alike.

Conclusion

In conclusion, the analysis of the global financial markets as of October 24, 2025, reveals a landscape marked by both challenges and opportunities. Throughout this overview, several key themes have emerged, reflecting the ongoing volatility and dynamic nature of financial conditions worldwide. Major markets are experiencing fluctuations driven by various factors such as economic indicators, geopolitical tensions, and shifts in monetary policy. These elements interplay significantly, shaping market sentiment and investor behavior.

The impact of interest rate adjustments by central banks continues to be a focal point, influencing capital flow and asset valuations across different regions. Investors should remain particularly vigilant regarding these developments, as they can have profound implications on investment strategies. Moreover, the current market sentiment suggests a cautious approach, with many traders opting for diversification and risk management techniques to navigate this uncertain environment.

Furthermore, staying updated on global economic trends remains crucial for stakeholders in the financial market. As new data comes to light, including employment rates, inflation levels, and GDP growth forecasts, market participants must be prepared to adapt their strategies accordingly. To enhance their decision-making processes, investors should also consider the effects of technological advancements and changing consumer behaviors, which are reshaping sectors and creating both risks and opportunities.

Overall, the landscape as of late October 2025 underscores the importance of agility in investment approaches. By continuously monitoring market developments and adjusting strategies in response to new information, traders and investors can better position themselves to thrive amid the inherent uncertainties of the global financial markets.

You might also like:

- Understanding Market Reactions to Macroeconomic Signals: The Role of the Federal Reserve and Upcoming Jobs Reports

- Navigating the Recall Token Market: Trends and Insights for Today

- FTSE MIB Sees Positive Growth as Energy and Defense Stocks Rally

- Chelsea Stuns Barcelona with a 3-0 Victory: Estevao Shines

- Han Sara Shines at Korea Top Brand Awards 2026: A Rising Star Among Legends