Introduction to the Stock Market Climate

As of October 22, 2025, the European stock market finds itself navigating a complex landscape characterized by mixed trends. Investors are currently exhibiting a cautious approach, significantly influenced by a variety of global economic conditions. Factors such as geopolitical tensions, fluctuating energy prices, and varied economic data from key markets have all contributed to an atmosphere of uncertainty, which is palpable across the various stock exchanges in Europe.

In recent months, market indices have shown signs of volatility, reflecting the broader challenges that economies worldwide are grappling with. The ongoing impacts of previous recessions, along with changes in monetary policy by central banks, have left many investors reassessing their strategies. These developments have led to a divergence in stock performances across different sectors; while some have thrived amid the uncertainties, others have struggled to maintain stability.

The current atmosphere is marked by heightened awareness of external factors, including the repercussions of international trade negotiations and the ongoing shifts within the global supply chain. This environment places immense pressure on corporate earnings and investor confidence alike, compelling traders to adopt a more analytical stance in their decision-making processes. Economic indicators such as inflation rates, employment figures, and consumer spending habits remain focal points for analysts, who are closely monitoring how these elements will influence stock valuations moving forward.

Overall, the European stock market climate as of October 2025 serves as a testament to the intricate balance between opportunity and risk. Investors must remain vigilant and informed as they traverse this landscape, ensuring they are equipped to respond strategically to the prevailing challenges and opportunities that define the current market conditions.

Understanding Mixed Trends in the Market

Mixed trends in the stock market refer to a scenario where some sectors or stocks experience gains while others may decline, creating a complex environment for investors. This phenomenon frequently manifests during periods of economic uncertainty and reflects underlying investor sentiment and market volatility. As investors navigate these varied trajectories, understanding factors contributing to such mixed trends becomes crucial.

One primary factor often influencing mixed trends is the performance of key economic indicators. Macroeconomic data, such as GDP growth rates, unemployment figures, and inflation metrics, can evoke divergent reactions among investors. For instance, if a country reports economic growth yet simultaneously faces rising inflation, investors may respond unevenly, leading to gains in certain sectors while causing declines in others. This divergence underscores the importance of discerning how economic news is perceived by market participants, as sentiment can pivot rapidly from optimism to caution based on new information.

Geopolitical events also play a significant role in determining market trends. Fluctuations arising from political instability, trade negotiations, or international conflicts can exacerbate investor apprehensions, resulting in mixed responses across the market. For example, amid escalating tensions in a particular region, energy stocks might benefit from rising oil prices, whereas technology stocks could suffer due to increased fears related to global supply chains. Such dynamics exemplify how external factors can simultaneously bolster and hinder different market segments, cultivating a mixed trend scenario.

In summary, the presence of mixed trends within the stock market illustrates the complexity of investor sentiment and the multifaceted influences of economic indicators and geopolitical developments. By closely monitoring these factors, investors can better understand and navigate the vagaries of market volatility, positioning themselves advantageously amid uncertain landscapes.

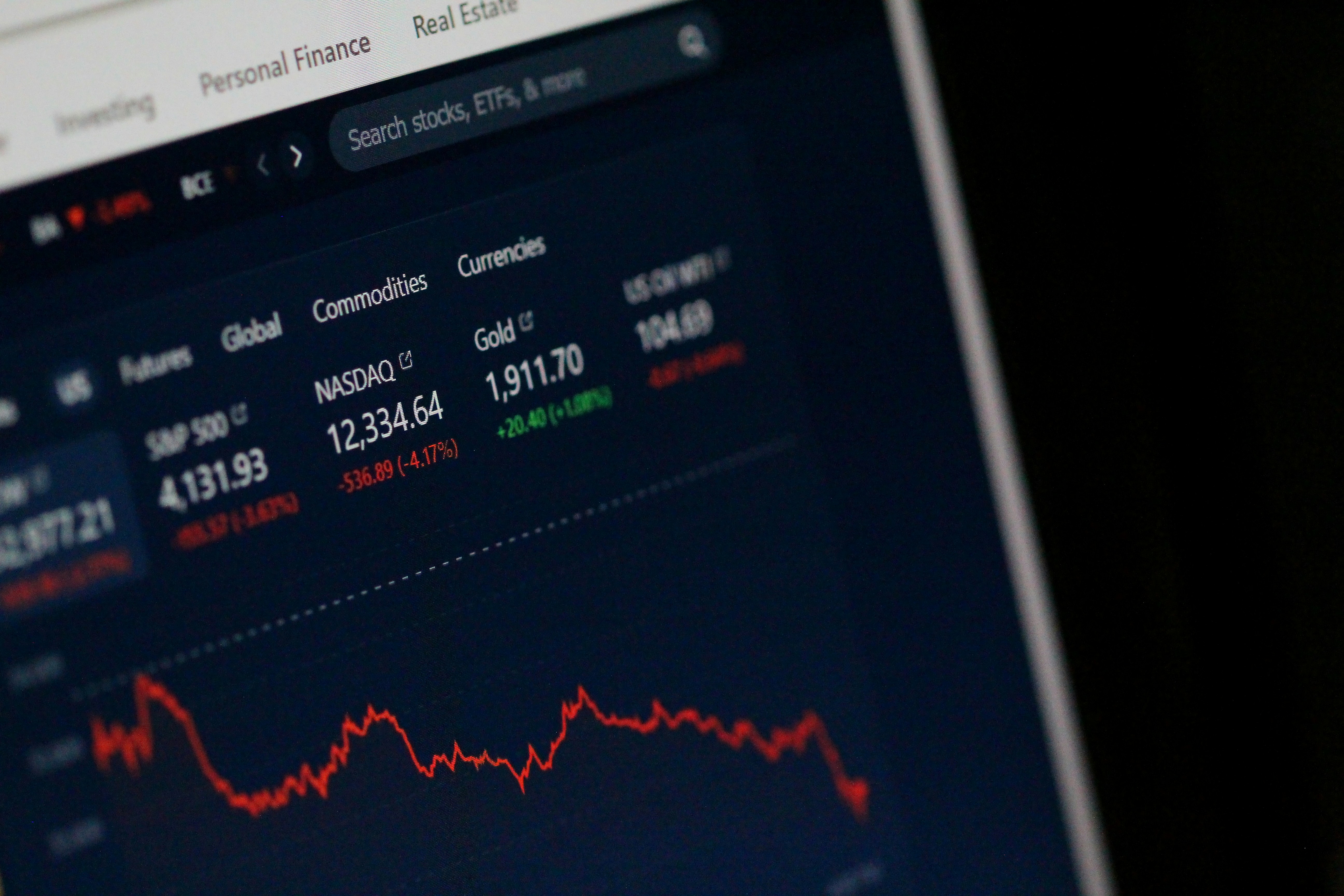

Stoxx 600: Performance Overview

The Stoxx 600, a key benchmark for European equities, experienced a minor decline of approximately 0.21% on October 22, 2025. This slight downturn reflects a period of mixed performance across various sectors within the index, which encompasses 600 large, mid, and small-cap companies across 17 European countries. Several factors contributed to this marginal decrease, impacting investor sentiment and market dynamics.

One of the primary influences behind the Stoxx 600’s performance was the ongoing fluctuations in global economic conditions. Uncertainties surrounding inflation rates, central bank policies, and geopolitical tensions have continued to weigh on the market. Notably, revelations regarding potential interest rate adjustments by the European Central Bank have left investors cautious, prompting a reevaluation of portfolios amidst a climate of volatility.

Sector-wise, the decline was primarily driven by weaknesses in the technology and consumer discretionary sectors, which have historically played vital roles in underpinning the index’s growth. Companies involved in technology were met with mixed earnings reports, raising concerns about future profitability in a landscape where innovation is critical. Similarly, consumer discretionary stocks faced pressure as changing consumer behaviors and economic fears hampered spending growth.

Despite the slight decrease, it’s important for investors to contextualize the Stoxx 600’s performance within a broader trend. Many analysts still express optimism regarding the underlying resilience of European markets. Factors such as a potential rebound in consumer confidence and ongoing recovery measures aimed at stabilizing economies across Europe could signal opportunities for growth, counterbalancing the recent fluctuations. Thus, investor vigilance remains crucial as the Stoxx 600 navigates through these challenging but potentially transformative times.

DAX: Germany’s Positive Trajectory

The DAX index, a critical benchmark for the German stock market, demonstrated a notable increase of approximately 1.82% on October 22, 2025. This growth reflects the robust performance of various sectors within the German economy, contributing to a sense of optimism among investors. The positive trajectory of the DAX can be attributed to several key components, including strong contributions from technology, automotive, and industrial sectors, which collectively represent a significant portion of German GDP.

Several leading companies in Germany played a pivotal role in this upward movement of the DAX. Notably, large-cap firms such as Siemens and Volkswagen reported impressive earnings, exceeding market expectations and bolstering investor confidence. Siemens, for instance, benefited from ongoing demand for advanced manufacturing solutions, while Volkswagen saw increased sales driven by its electric vehicle lineup. Such performance highlights the resilience of these companies in adapting to market demands and investing in future growth, which subsequently reflects positively on the broader index.

The current state of the DAX is not just a representation of corporate growth but also a barometer of the overall economic health of Germany. An uptick of this magnitude suggests that the economy is recovering and shows potential for future expansion. Furthermore, the positive momentum in the DAX serves as an indicator of investor sentiment, with many now anticipating sustained growth as key sectors continue to innovate and evolve. As Germany positions itself within the global economic landscape, the performance of the DAX will remain a crucial indicator of its financial stability and economic prospects going forward.

FTSE 100: Insights into the UK Market

The FTSE 100 index, which represents the performance of the largest 100 companies listed on the London Stock Exchange, experienced a slight decrease of approximately 0.86% on October 22, 2025. This decline can be attributed to several factors influencing investor sentiment and market dynamics within the UK economy. A combination of geopolitical uncertainties, potential changes in monetary policy, and fluctuations in commodity prices have played a significant role in the recent market behavior.

One of the key contributors to the downturn was speculation surrounding interest rate adjustments by the Bank of England. As the central bank deliberates on its next move, market participants have responded with caution, leading to a pullback in stock prices. Furthermore, global economic pressures, including ongoing trade tensions and inflation concerns, have also heightened uncertainty, which in turn affects investor confidence in the UK market.

Analysts have noted that sectors heavily weighted in the FTSE 100, such as energy and financial services, have been particularly sensitive to these external factors. For instance, volatility in oil prices has directly impacted energy stocks, while banking shares have seen a decline due to fears of potential regulatory changes and economic slowdowns. Although the overall performance of the FTSE 100 remains diverse, the recent dips in these vital sectors suggest a cautious outlook for investors focusing on the UK market.

As investors assess the implications of the FTSE 100’s performance, it is essential to consider both short-term volatility and long-term prospects. The current environment presents opportunities and challenges, requiring a strategic approach for those looking to navigate the complexities of the UK equity market. The anticipated changes in monetary policy and the broader economic landscape will undoubtedly continue to shape the performance of the FTSE 100 in the coming months.

CAC 40: A Sideways Movement

The CAC 40 index, which is a benchmark for French equity markets, has exhibited notable fluctuations recently, characterized by a relatively stable sideways movement. Specifically, during the analyzed period around October 22, 2025, the index demonstrated slight variations, oscillating approximately 0.18% above and below its reference level. This nominal change suggests a market environment that is marked by uncertainty and a pause in decisive trends among investors.

Such a sideways movement can often reflect underlying economic conditions or investor sentiment regarding future market performance. In the case of the CAC 40, these small fluctuations indicate a cautious approach from market participants. Investors may be awaiting additional economic data, corporate earnings announcements, or geopolitical developments that could influence market direction. The stability seen in the index may also suggest a balance between buying and selling pressures, as participants weigh the potential risks and rewards of investment in the French stock market.

Furthermore, the sideways movement of the CAC 40 has implications for various sectors within the French economy. Sectors that typically drive the index, such as technology and healthcare, may be experiencing contributing factors affecting investor confidence. This includes fluctuating economic indicators, such as GDP growth rates or inflation figures, which can heavily influence stock performance. While the minor changes might not seem significant at first glance, they are crucial in understanding the broader health of the French market.

Overall, the observed movements of the CAC 40 index during this period illustrate an equity market that remains in a state of cautious equilibrium, as investors digest information and consider their positions in the face of evolving economic landscapes. The direction that this index ultimately takes will be closely monitored, as it serves as a vital indicator of market trends in France.

Comparative Analysis of European Indices

The European stock market comprises various indices, each representing distinct economic sectors and geographical realities. As of October 22, 2025, the performance of these indices illustrates notable disparities, shaped by diverse factors such as economic policies, geopolitical developments, and market sentiment. Among the prominent indices, the DAX in Germany and the FTSE 100 in the United Kingdom serve as crucial indicators of their respective economies, showcasing varying trends.

The DAX has exhibited robust growth, buoyed by a strong manufacturing sector and Germany’s status as a leading exporter. This growth is largely attributed to Germany’s investment in green technologies and substantial infrastructure projects, supporting an uptick in capital expenditure. Conversely, the FTSE 100 has faced challenges, influenced by ongoing uncertainties around Brexit and economic slowdowns. The British index includes several companies heavily reliant on international trade, which may have constrained its performance in comparison to its continental counterparts.

Further highlights arise from the CAC 40 in France and the IBEX 35 in Spain. The CAC 40 has shown favorable performance through strong banking and consumer sectors, benefiting from political stability and reform initiatives aimed at enhancing economic resilience. Meanwhile, the IBEX 35 has been hampered by high unemployment rates and political fragmentation, leading to variable investor confidence.

Market analysts suggest that continued fluctuations may occur due to external shocks such as inflationary pressures and monetary policy adjustments by central banks in Europe. The divergence among these indices underscores the necessity for investors to consider not only macroeconomic indicators but also regional dynamics when making investment decisions. As the European stock market evolves, close attention to these developments may yield significant insights into future trends and opportunities.

Investor Sentiment and Market Dynamics

The European stock market has historically been influenced by various factors including economic indicators, geopolitical events, and investor sentiment. As of October 22, 2025, the prevailing investor sentiment plays a pivotal role in shaping market dynamics. Investor sentiment is primarily driven by the collective mood and psychology of market participants, which can effectively sway trading behaviors and impact overall market performance.

Recent observations indicate that a cautious yet optimistic sentiment has emerged among investors. This change can be attributed to several factors including positive earnings reports from key corporations and stabilizing economic indicators within the Eurozone. Investors are increasingly looking towards market fundamentals, assessing the long-term growth potential rather than succumbing to short-term volatility. This shift in mindset has instigated a more measured trading approach, leading to a moderate trend in stock prices across various sectors.

Moreover, market dynamics are also influenced by ongoing geopolitical developments, particularly the negotiations and agreements that affect trade relationships within Europe. Investor reactions to such political nuances can lead to fluctuations in market indices. For example, during periods of uncertainty or tension, a risk-averse behavior is commonly observed, resulting in increased demand for safe-haven assets. Conversely, moments of clarity and stability often foster a return to risk-seeking behavior, where investors are willing to allocate capital towards more volatile securities.

In essence, the relationship between investor sentiment and market dynamics is integral to understanding the European stock market landscape. Awareness of these factors allows investors to make informed decisions as they navigate through the complexities of the market environment. By keeping an eye on sentiment indicators and remaining vigilant to these influences, participants can better position themselves to respond proactively to the evolving market conditions.

Future Outlook for European Indices

As we look ahead to the potential trajectory of European stock market indices, several critical factors warrant consideration. The economic landscape in Europe remains dynamic, influenced by both domestic policies and international developments. Analysts have been observing trends that may shape future performance, including interest rate adjustments by the European Central Bank (ECB), geopolitical tensions, and the overall health of major economies within the Eurozone.

Current market dynamics suggest that while there are challenges, opportunities for growth are also present. Inflation rates, which have been a concern, appear to be stabilizing. The ECB’s monetary policy adjustments could play a pivotal role in shaping investor sentiment. If rates continue to remain steady or decrease, we might anticipate a more favorable environment for equities. Additionally, the rollout of fiscal stimulus across various European nations is expected to bolster economic activity, potentially leading to increased corporate earnings and consequently supporting stock indices.

Geopolitical factors cannot be overlooked, as they often present both risks and opportunities. The ongoing situation with multiple regions may lead to volatility, but they might also encourage market reallocation, causing investors to seek out stronger performance sectors. Furthermore, technological advancements and a focus on sustainability are likely to drive demand in specific industries, influencing indices positively.

Looking specifically at the prediction for the next few months, a moderate growth scenario seems feasible, provided that external shocks do not derail the current trajectories. Seasonal factors typically play a role in market behavior, and historical trends in the fall months suggest potential for gains. Nevertheless, investors should remain vigilant, staying attuned to both macroeconomic indicators and global events that could impact the European stock market environment.